AIM13 Commentary - 2016 Q1

“If you don’t know where you are going, you’ll end up someplace else.”

- Yogi Berra

May 20, 2016

Dear Investor,

By one measure at least, the first quarter was rather uneventful in the markets. The S&P 500 Total Return (the “S&P 500 TR”) gained a modest 1.35%. We have noted before under similar circumstances that had you gone to sleep on January 1st and woke up on April 1st and read that headline, you would have thought all is well in the equity markets. Unfortunately, all is not well. During the quarter, the market slumped about -10.3%, which technically qualifies as a “correction,” before regaining that ground, and more, before quarter end. In fact, it was the first quarter since 1933 for the S&P 500 TR to be down more than 10% during the quarter and yet still finish in the green.

Expressing the frustration of many in the industry, Dan Loeb, the well-known hedge fund manager who runs Third Point Capital, said that he believed the first quarter was “one of the most catastrophic periods of hedge fund performance that we can remember since the inception of this fund [in December 1996].” He predicted a “killing fields” for hedge funds (albeit one where he sees opportunity).

Following an awful three months, hedge funds have deservedly received a public lashing in the press. One group, known as the Hedge Clippers, claimed on social media recently that hedge funds’ investments in fossil fuel producers have the effect of causing cancer. Dealbreaker even equated hedge funds to Apartheid. Other recent headlines about hedge funds include:

Buffett says hedge funds are

a bad deal for investors.

- Yahoo News

HEDGE FUNDS UNDER SIEGE

- ValueWalk

‘Let them sell their summer homes’: NYC pension dumps hedge funds.

- Reuters

Hedge funds are already dead…

they just don’t know it yet.

- Dealbreaker

Hedge fund fee attack:

Paying money to lose money?

- Bloomberg

CalSTRS CIO: “The 2 and 20

hedge-fund model is dead.”

- CNBC

If you are now expecting an impassioned defense of hedge funds, you may be surprised to hear that we agree wholeheartedly with most of the criticism of the industry as a whole. Although we have been investing in hedge funds for many years, we have never seen the strategy face such an existential threat as we see today. We stand shoulder to shoulder with most of the critics. In fact, we feel a little like Peter Finch playing Howard Beale in the 1976 movie classic, Network:

“I want you to get up right now, sit up, go to your windows, open them and stick your head out and yell - 'I'm as mad as hell and I'm not going to take this anymore!' Things have got to change. But first, you've gotta get mad! You've got to say, 'I'm as mad as hell, and I'm not going to take this anymore!' Then we'll figure out what to do about the depression and the inflation and the oil crisis. But first get up out of your chairs, open the window, stick your head out, and yell, and say it: "I'M AS MAD AS HELL, AND I'M NOT GOING TO TAKE THIS ANYMORE!"

- Howard Beale, Network, 1976

Yes, we are mad as hell about hedge funds, and we know we are not alone. According to The IDW Group, this past quarter was the worst net withdrawal period for hedge funds since the end of the financial crisis. “It’s a performance industry,” said Anthony Lawler of GAM, the asset manager, as reported in The Economist. “If you don’t perform, people take their money and leave.” In February, normally one of the biggest months for hedge fund inflows, a scant $4.4 billion was raised, a six-fold decrease from the average of $23 billion raised in the month of February from 2010 to 2015. Fund launches are also way down: according to Hedge Fund Alert, the 544 initial Form D’s hedge fund managers filed with the SEC in the first three months of this year were the fewest since the 2008 market crash.

Likewise, hedge fund closures remain at historic highs, even on the heels of 2015 which was the worst year for hedge fund liquidations since 2009, according to Hedge Fund Research. Aurora Investment Management, which at one time managed over $14 billion in hedge fund investments, announced in April that it was shutting down following redemptions in the wake of its attempt to be bought by a Northern Trust affiliate. At the end of the year, BlueCrest Capital Management, a hedge fund firm that managed nearly $38 billion at peak, closed shop and returned over $7 billion to investors. Its founder, Michael Platt, told Forbes at the time that “ongoing secular changes in the industry, including trends in fee levels, the cost of hiring the best trading talent, and the challenges in tailoring investment products to meet the individual needs of a large number of investors, have weighed on hedge fund profitability.”

While we do not believe that hedge funds are dead, they do have some serious problems:

Major Problem #1: Focusing Too Much on Asset Gathering. Simple math illustrates the point: a manager who charges 2% and 20% with $1 billion in AUM can generate $20 million in management fees annually and, if he performs well (say, posting a 20% gross return), his 20% performance fee generates another $40 million, netting him $60 million for his work. However, that same manager is more incentivized to grow his AUM to $3 billion. Then his management fee alone will net him the $60 million – and he doesn’t even need to generate any returns for his investors. Speaking at the Milken Conference recently, Steve Cohen said, “It’s very hard to maximize returns and then maximize assets.” We could not agree more. At one time, hedge fund managers set asset size targets based on levels where they could generate the highest returns for their limited partners. This made sense: the manager would typically put most of his liquid net worth in the fund and he made more on returns than on fees. Now, however, it is about finding the intersection of the highest asset level with the most muted returns large investors are willing to accept.

Major Problem #2: Trading the Same Names. Too many managers chasing the same names is a recipe for disappointing returns. Shire, Valeant and Pfizer/Allergan have all been hedge fund graveyards. Hedge fund managers need to go back to their roots: finding underfollowed investment ideas. We saw recently that an index that tracks the mostly highly concentrated holdings of equities by hedge funds has plunged 45% from July 2015 through the end of February 2016, according to Novus, the data aggregator. Peter Lupoff, writing in Seeking Alpha, noted that this is the worse relative performance for the group since at least 2005.

Major Problem #3: Focusing Too Much on Building a Business Rather than on Investment Returns. This problem manifests itself in a variety of ways:

- Being too cautious and afraid of a drawdown that will scare away “institutional” investors like large pension funds;

- Focusing on short term results, day to day or month to month, when long term investors are more focused on five, ten, and fifteen year returns;

- Meeting investor demand for better liquidity (e.g., monthly withdrawals), which only compounds the problem of focusing on short term results;

- By focusing on short term returns, in a low return environment, some managers are also chasing higher risk and sometimes less liquid opportunities, essentially “painting themselves into a corner” which only a Hail Mary bet can rescue them from; and

- Spending more time running the business rather than running the money – hiring and firing, opening remote offices, communicating with current and prospective investors, etc.

How do we address these issues? As our investors know, we regularly underwrite our own investment program in hedge funds, spending more time on our current managers than on finding the next great untested star. At the risk of repeating ourselves, we can summarize what we look for in our own managers and how we factor in these troubling trends in the industry generally:

- Why does a manager get out of bed in the morning? If it is not about making money from returns rather than fees, we want no part of him or her.

- How aligned are the manager’s interests with the investors? If a manager’s interests are not aligned with ours, no matter how smart they are, at the end of the day, investors will be on the losing end. Like the best run casino, in the long run the house will always win and the patrons will always lose. The regrettable fact about the casino analogy is that, by the time investors realize they are playing a losing game and suffer losses, the manager has collected its annual incentive fees. Heads they win, tails you lose!

- Does the manager know how to short? Only managers who recognize that there is still a spread between the best stocks and the worst stocks, who do not just “hedge” by buying index shorts, can make money in down markets and protect capital.

- How does the manager think about risk management? One of our best long term performing managers is perfectly comfortable carrying large exposures of cash when the opportunity set is simply inadequate to deploy capital.

- Is the manager spending more time on the portfolio or on the road raising money and on TV getting publicity? Enough has been said about this here, but it remains the biggest red flag of all.

You may notice that we do not mention fees. It is not because we do not care about fees. We certainly do. However, we think the headlines about fees are missing the full story. Many managers in the industry get around the fee issue by exploiting expense provisions to charge anything and everything to the fund. The most egregious of these include salaries, technology, private planes, etc. At the end of the day, it really is not about the amount of fees we pay – in fact, if we are paying a performance fee that means the manager is performing. We focus on the net returns considering the amount of risk taken.

We do recognize that complaining about lower returns for truly hedged strategies in the tail end of a seven-year bull market fueled by central bank policies may be misplaced. In fact, given that the average hedge fund net exposure ranges from about 30% for all hedge fund strategies to about 50% for equity long/short strategies, hedge fund returns since the financial crisis have not been particularly bad. We will talk about appropriate expectations for investments below, but keeping apace an unprecedented run in equities was never a mandate for hedge funds. We also recognize that the journalists who proclaim the demise of hedge funds bear no small measure of schadenfreude – that is, pleasure derived from another person’s misfortune. What better target than a hedge fund manager?

This is not the first time pundits have said the industry is on life support. To paraphrase Mark Twain, the reports of the death of our industry may be greatly exaggerated, as we have seen these headlines before:

- Investors Fall out of Love with Hedge Funds, Financial Times, October 2012

- Hedge-Fund Hemorrhage, Marketwatch, April 2008

- Hedge funds: It’s survival of the fittest as record numbers close, Independent, October 2006

- Hard Times Come to the Hedge Funds, Fortune, January 1970

Serious problems do exist, and hedge fund managers need to respond. However, more importantly, investors need to chart a course through challenging markets and these industry cross currents, finding a way to best deploy investment capital to achieve their objectives.

Where do you go from here?

We chose the Yogi Berra quote above because it forces the central question investors need to ask themselves: What are my return expectations? Equally, in a low interest rate, low return environment, are my return expectations realistic? Unfortunately, there is no such thing as a fat free Big Mac. Human beings, however, are not always the most realistic creatures. The fact that, according to studies, 95% of us view ourselves as above-average drivers should tell you something. Moreover, investors are as prone to irrational expectations as anyone.

So we would like to ask all of those people who are complaining about hedge funds, where are you putting your money to work these days, seven years into a bull market? And what risk are you taking? We define risk as taking your whole net worth to the top of the Empire State building and being prepared to throw it off; i.e., permanent capital loss. With that definition in mind, where do you go from here?

Today, after the stock market has gone straight up for five years, investors are faced with two extremes: Go into cash and wait for the market crash or a correction and then go all in at the bottom, or else ride this bull with both feet in the stirrups, but try to jump off before it rolls over on you, no matter how quickly that happens.

- Tyler Durden, Zerohedge

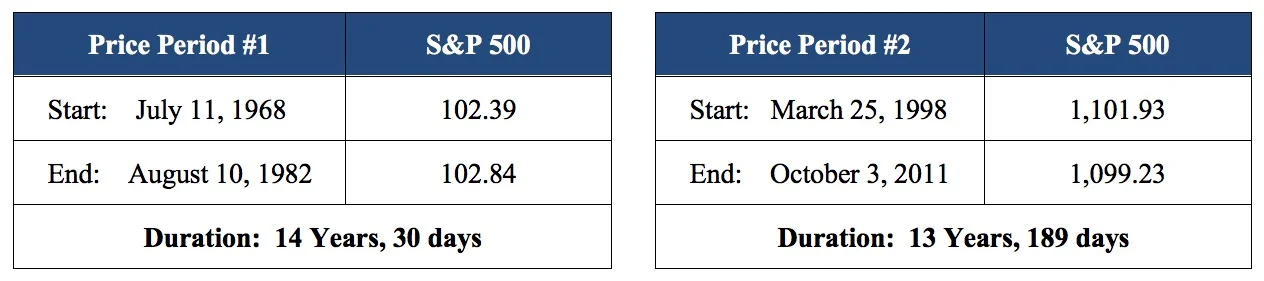

Long Only Equity? We are committed to absolute net returns to our investors over the long term, and as such we are not normally ones to compare hedged strategies to other asset classes. However, while we greatly respect Warren Buffett, we disagree with his suggestion to put all of your money in low cost index funds. If you invested in the S&P 500 TR in January 2000, through the end of the first quarter 2016, you would have earned a modest 4.0% annual return. In fact, in two times in our lifetimes alone, we have had extended periods of zero growth in the S&P 500:

Two Periods in the Last Fifty Years of Zero Growth in the S&P 500

Given the risk of long term minimal returns, we disagree that someone should put all of their savings into S&P 500 index funds. Aside from low returns, there is the risk of a permanent loss of capital. J.P. Morgan released a report in mid-February that concluded there is a 92% chance of a recession starting within three years. The probability of a recession within two years is 67%. The authors pointed to declining corporate profit margins, noting that 9 of the last 11 times margins have fallen this far, a recession was "underway or would begin within a few years.” Of course, there is also Donald Trump, who predicted in early April that the U.S. economy is on the verge of a “very massive recession.” Not surprisingly, we read recently that now only 52% of American adults have money in the market, either in individual stocks or through 401k plans. That is down from 65% in 2007. We also were taken aback to read in the Wall Street Journal that the projected rise this year in the global cost of healthcare benefits now stands at 9.1%, a startling high rate of increase in the context of an already weak economy.

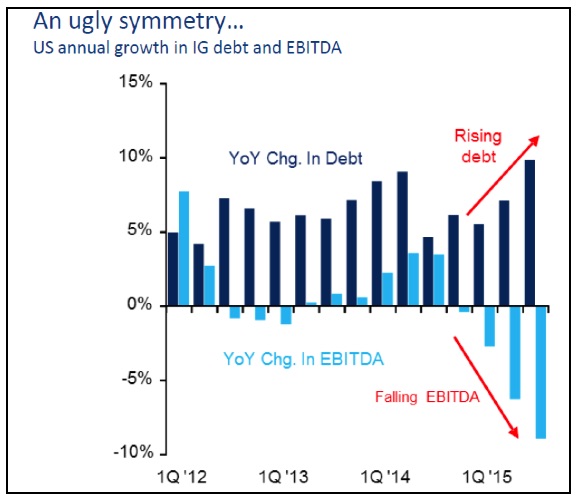

Troubling trends facing equities are not hard to find. One we came across from the Milken Institute’s annual gathering in early May that is particularly disconcerting:

Comparing Investment Grade Debt and Corporate Earnings

Source: Milken Institute, Citi Research, Factset, Citi Fixed Income Indices

According to a recent UBS research report, the current rally, which on April 29th stood at 2,611 days, is now the second longest in modern history, behind only the 1990-2000 bull market. While the VIX has returned to low levels following a spike in volatility in February, the chart below indicates a distinct uptick in overall volatility in the last six months:

Source: J.P. Morgan

We often look for indicators off the beaten path to give us some insight about the direction of the equity markets. We read recently that more than 40% of student borrowers are not making their payments, according to the Wall Street Journal. In another data point, Harry Dent, writing in Seeking Alpha, pointed us to an interesting statistic in February: the Restaurant Performance Index. As the index has now fallen below the 100-level line, restaurants are officially in a period of contraction. The index fell to a negative reading of 99.7 in December from 101.3 in November alone, a 1.6% drop in just one month. That is the biggest drop since late 2007.

Another obscure but perhaps telling indicator of negative things to come was picked up by Trusted Insight in May, which reported that sales of ping pong tables in Silicon Valley have plunged fifty percent in the first quarter of this year, according to a wholesaler in San Jose.

What about fixed income? Some people view hedge funds as a bond substitute. This makes us scratch our head, as the 10-year bond is currently yielding about 1.75%. Leaving aside the prospect of low returns for the foreseeable future, there is also enormous risk in fixed income from a liquidity and credit perspective. We have also been watching the strange phenomenon of negative interest rates. The Wall Street Journal reported that at the end of February, 23% of the debt in the Merrill Lynch Global Fixed Income Markets Index had a negative yield, up from just over 13% at the start of the year. Almost unbelievably, approximately $7 trillion in sovereign debt had negative interest rates in the first quarter. Lest anyone has any doubt about the unprecedented run in low interest rates, the chart below clearly tells the story:

Commodities? Commodities prices suffered enormously in 2015 as growth in China slowed. For instance, oil prices dropped by 47%. At the same time, the correlation between oil and stocks reached its highest since 1980. This year looks no better: according to The Diplomat magazine, all of the World Bank’s main commodity price indices are expected to drop this year due to “persistently large supplies, and in the case of industrial commodities, slowing demand in emerging market economies.”

Real estate? We are reminded of the recent boom in real estate here in Manhattan every time we look up and see the tower of 432 Park Avenue, where the average price per square foot is a stunning $6,894, standing head and shoulders above almost every other skyscraper in mid-town. The building is over 70% sold, but closings have plateaued, according to a report on CNBC in March. Nationally, things are not much better: the number of real estate contracts signed in January and February fell more than 20 percent from a year earlier to their lowest levels since 2009, according to real-estate analytics firm UrbanDigs.com. Expensive apartments are sitting idle for roughly 90 days before being sold, the longest "time on market" since January of 2013, according to the StreetEasy Blog. Building permits in March missed expectations by the widest margin since at least 2002.

* * *

We understand the frustration with hedge funds, but we also recognize the need to know where you are going and to be realistic given the opportunity set. Hedge fund investors are right to be unhappy with returns. However, they also must understand that you cannot put trillions of dollars into an industry where size is the enemy of performance and then expect outperformance. Hedge fund managers will collect management fees all day long if investors allow it. To those who complain about these asset-gathering hedge fund managers, we say, you reap what you sow!

You also cannot drive forward by looking in the rearview mirror. Investors need to look forward and, even when it is foggy, to chart a path to achieve their realistic objectives. Without knowing where you are going, as Yogi Berra put it so well, you do not have a good chance of getting there. Unfortunately, a lot of people’s expectations and how they measure satisfactory performance are just plain wrong.

Readers of our letters know that we are big fans of Chevy Chase. One exchange from Caddyshack captures the problem nicely:

Judge Smails (Ted Night): Ty, what did you shoot today?

Ty Webb (Chevy Chase): Oh, Judge, I don't keep score.

Judge Smails: Then how do you measure yourself with other golfers?

Ty Webb: By height.

- Caddyshack, 1980

We continue to believe that, for the majority of our portfolio, we must allocate our capital and our partners’ capital to the very best hedge fund managers, who we believe can achieve our objectives: given the risk taken, outperformance relative to other strategies over the long term.

What Keeps Us Up At Night

There are no easy answers for all of the risks and trouble, in markets and in daily life, that we all face. Some people just choose to leave and find greener pastures elsewhere. A friend shared with us the chart below regarding the ever increasing number of Americans renouncing their U.S. citizenship:

While we have no present intention of leaving the country (where would we go?), we do find ourselves coming back to a small handful of deeply unsettling things that we are forced to live with in our daily lives:

Cyber Attacks: In April, we brought together a small group of cybersecurity professionals in our network to share ideas and insights about the explosion of cyber threats in our industry, in finance, and even in our own personal lives. There were sixteen of us at the table, including information security experts from the largest banks and consulting firms. Todd Feinman, CEO of Identity Finder, provided a fascinating overview of how corporations store so much data containing our personally identifiable information or “PII” and how data breaches often leak that sensitive information to countless places on the Internet – and ultimately into the hands of cyber criminals. Todd is a former “ethical hacker,” whose experience worming his way through company security firewalls and into power grids, public transportation controls, and even lottery computer systems makes him someone you want working for the good guys (thankfully, he does). We came away smarter and even more scared.

Last quarter, we shared a piece on Freezing Your Credit. This time we would like to tell readers of the importance of dual factor authentication, or using two separate login protocols to access sensitive information over the Internet. Everything from bank accounts to Gmail and even LinkedIn are implementing this second layer of defense. We recommend taking the time to learn more about how this relatively simple control can thwart many cyber attacks.

Terrorism: We were deeply troubled by the reports coming out of Belgium that Salah Abdeslam, one of the primary suspects of the Paris attacks that left 130 innocent people dead, had apparently been gathering information about a nuclear research facility in Germany. In response, it was reported in late April that Belgium is giving everyone living within a 100-kilometer radius of its nuclear reactors an iodine pill. Iodine pills protect the thyroid gland from absorbing radioactive iodine. The threat of a terrorist attack on our critical infrastructure is one of the scariest terrorist scenarios we can contemplate. We have noted previously the attack on the San Jose power substation in April 2013. At the end of December, the Wall Street Journal first reported a previously unpublicized attempted attack by Iranian hackers on the Bowman Avenue Dam near Rye Brook, New York. Apparently, this was just a test run. Vigilance and being realistic about these threats cannot be overemphasized.

We thank you for the confidence you have placed in us and welcome any questions or thoughts you may have.

Sincerely,

Alternative Investment Management, L.L.C.