AIM13 Commentary - 2025 Q4

“Always behave like a duck — keep calm and unruffled on the surface but paddle like the devil underneath.”

When we began this journey more than 25 years ago, our focus was intentionally simple and has remained unchanged through cycles, opportunities, and challenges. From day one, our objective has been to remain disciplined and stay focused on our three core principles:

First, to invest our own capital across a range of strategies to compound capital over time, taking only an acceptable and well-understood amount of risk;

Second, to create structures where alignment of interest is paramount – where we truly benefit only if we perform, and where outcomes are shared alongside our partners; and

Third, to avoid chasing business opportunities that fail to meet our standards set by the first two principles, regardless of how attractive they may appear in the moment.

We live in a time of great uncertainty and risk. The war in the Middle East and its economic and geopolitical impacts (not to mention the tragic hardships and loss of life), the disruption of AI, and political turmoil here and abroad are just a few of the many things that keep us up at night. Amidst all of this, we continue to do what we have always done: remain calm, keep a close eye on our current investments, and work hard to find new opportunities often hidden in the chaos of our times. Above all, we do not panic. As we too often say, the good thing about always being bearish is that you are never wrong, just early.

* * *

Our focus has always been on our current investments. While we are seeing a tremendous amount of new opportunities, we work hard to kill most of them quickly so that we can spend more time on our current investments. We are always judicious around accepting and deploying new capital. In fact, we recently once again returned some capital from one of our entities. We have also reduced the number of hedge funds that we are invested in, which increases the average amount of time we can spend on each current investment.

Only a select few new investments make it through our funnel. Since January 2024, we have made on average about one new investment a month in direct deals, hedged and private equity funds, private credit, and venture strategies. Some examples of uniquely compelling areas we have invested in recently include:

Nuclear energy and alternative fuels – Investments in this area include a company developing nuclear fuel, another building small, portable nuclear reactors, and a third refining soybean and used cooking oils into renewable diesel.

Advanced technologies supporting the AI industry – We avoid the speculative areas around AI where valuations make investing more like gambling than anything else. However, we have found compelling risk adjusted return opportunities in next generation chip fabricators and in the datacenter cooling space, all designed to meet the enormous demands of the growth in AI.

Drones and related technologies – We first mentioned the opportunity in unmanned aerial systems in these letters back in early 2019. Since then, international conflicts have borne out the need for technologies across drone and counter-drone systems. Our investments here have included electro magnetic solutions to defeat drone swarms, tethered drones, and counter measures using both kinetic and radio frequency tools to take out hostile drones.

Roll ups in fragmented industries – Our investments here include roll-ups in the insurance brokerage and landscaping spaces, and a company acquiring HVAC wholesalers and distributors.

Healthcare technologies – Partnering with experienced and specialist managers in this space, we have invested in biotech in such areas as genetic data storage and synthetic gene creation. We believe the remarkable advancements here will not only provide great return opportunities but equally extend and save human life.

We are fortunate to be able to see these deals and share them with our partners. We have always believed that providing unique access to deals to our network further drives our deal flow. While we have been busy, we have not chased the craziness. We are not going to deviate from what we have always focused on: finding clearly differentiated, unique investment opportunities.

In private equity, we continue to see improvements in the M&A environment, with the number of new investments and realizations increasing each month. According to McKinsey’s 2026 Global Private Markets Report, released in February, in 2025, “The value of PE-backed exits globally surged … up more than 40% – aided by a nearly 100% increase in PE exit deal volume via IPO.” Anecdotal evidence from our managers is in line with these statistics.

While the deal environment has improved, there also have been many reports recently about private equity investors being disappointed with returns. For instance, earlier this month, the Ontario Teachers Pension fund reported that in 2025 its private equity investments lost -5.3%. By focusing on smaller managers doing “old school private equity” rather than on the larger funds, we believe we will outperform over time. In fact, we often see the larger PE funds buying from our smaller funds.

* * *

We have said before that too many people focus on assets under management as the best measure of success in our industry. Even as our own AUM approaches $2 billion, we remain committed to the same core principles we held 25+ years ago. This requires patience, conviction, and a constant commitment to our process. We strive to listen and to understand – not to simply respond – and to continuously challenge ourselves on where we may be wrong, where assumptions need to be tested, and where we can improve and do better.

“Every strike brings me closer to the next home run.”

We all make mistakes, but the key is to learn from them. Markets evolve, circumstances change, and humility is essential but discipline is non-negotiable. While our strategies have performed well recently, success, of course, can breed complacency if left unchecked. We will never succumb to complacency!

“Past performance is not indicative of future performance –

unless you are talking about one’s character.”

At the heart of everything we do is a simple belief: the first rule of investing is finding good people. Talent matters, but character matters more. Life is too short to cut corners—especially when it comes to integrity, trust, and long-term relationships. The quality of the people we work with, invest alongside, and entrust with responsibility ultimately determines the durability and success of our outcomes.

When we assess a person’s character, experience is one of the most important qualities we look for. Recently we noticed a trend emerging that suggested the average age of the hedge fund managers we partner with has been steadily increasing. That caused us to challenge ourselves why: Was it because we are getting older and have a bias towards managers that share (or are closer to) our age? Maybe. Or maybe it is because a 35-year old manager now was barely old enough to drive when in 2008 the market had its worst year since the 1930’s. Not that we will not invest with a manager born after 1990, but living through that teaches you a lot about markets.

The beginning of each year is always an opportunity to reflect on the responsibility that comes with managing capital and building enduring partnerships. We are grateful for the trust placed in us and do not take it lightly. To everyone who has been part of this journey – investment partners, colleagues, and our team – thank you for your trust, your candor, and your shared belief in doing things the right way. We look forward to continuing to build, improve, and earn that trust in the years ahead.

Market Observations

“It’s a very complicated case, Maude.

You know, a lotta ins, a lotta outs, a lotta what-have-yous.”

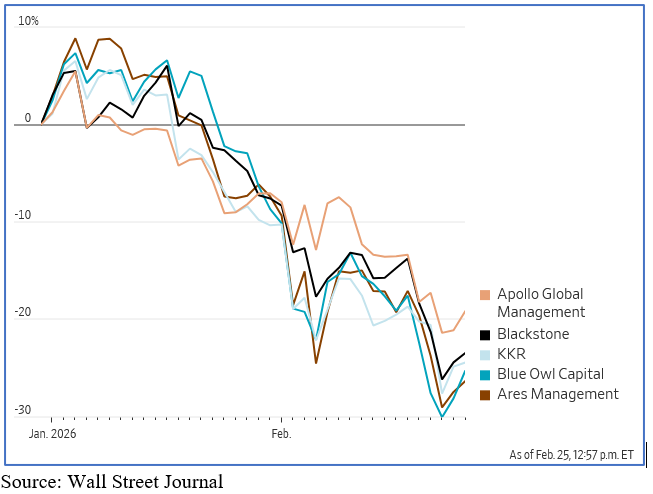

Private Credit Managers Limit Investor Redemptions. Blue Owl’s decision in February to effectively shut off regular redemptions in one of its retail-focused private credit funds and instead return capital over time through loan repayments and asset sales sent shock waves through markets. In private credit specifically, Blue Owl’s move reinforces the core tradeoff of the asset class – stable income in normal times, but limited liquidity in risk-off periods – and suggests investors may demand more transparency, tighter match-funding, and a bigger premium for locking up capital.

In classic run on the bank style, in late February private credit investor concerns sparked redemptions representing 9.3% of BlackRock’s HPS Corporate Lending Fund. The firm stuck to its 5% investor cap (in fact, this was the first time in the fund’s four year history that redemptions exceeded the cap). A few days later, Blackstone said it had received record withdrawal requests, representing 7.9% of its $82 billion fund known as Bcred. However, unlike BlackRock, Blackstone said that it would fulfill the redemptions after a number of senior Blackstone employees invested more than $150 million in the fund, as reported by Bloomberg News. Similar troubles more recently affected Ares, KKR, and Future Standard.

When the BlackRock news broke, its shares fell 7.2%. Not surprisingly private fund managers have taken a beating this year:

Year-to-Date Stock Performance of Major Private Fund Managers

(January 1 to February 25, 2026)

The freeze is a reminder that private credit offers higher yields partly because the underlying assets are illiquid, even when the product is marketed to wealth investors who expect some access to cash. This was less a sign of immediate systemic crisis than as a stress test of confidence: when investors ask for money back faster than managers can monetize loans, gates and asset sales can pressure listed alternative-asset stocks and widen skepticism around private-credit valuations.

One commentator on X framed it this way:

“Equity-like returns with downside protection. Low correlation to

public markets. Proprietary deal flow.

✋ And a gate… in case anybody gets any ideas.”

Devil in the Details. When we saw Paramount increase our streaming service subscription recently by about 40%, from $98.99 to $139.99, it reminded us of one of the most important things to remember when doing due diligence. Streaming platforms and other subscription-based services have gotten especially good at sneaking price increases past customers by spreading them out across annual renewals, bundling changes, premium-tier reshuffling, and quiet email notices that are easy to miss. A jump like Paramount’s shows how companies rely on customer inertia: once payment details are saved and the service is part of someone’s routine, many people keep paying without closely reviewing the new charge. The same can happen with investments. A “set it and forget it” mentality sets in and unscrupulous managers take advantage of it. Good investors focus as much on ongoing due diligence and what is in the fine print reported to them as they do on initial due diligence.

“A market that moves 3% on a blog is a market that does not know.”

The Impact of Artificial Intelligence – A “Known Unknown”. A doomsday AI research report issued in February by Citrini Research caused a huge market selloff when markets opened on the following Monday morning. Shares of IBM plunged 13%, its worst one day performance in 25 years. Companies in the payment space like AMEX, Visa and Mastercard, were hard hit, along with DoorDash and Uber, all named in the report as particularly vulnerable to AI. It later emerged that one of the co-authors, Alap Shah, was actually short a number of the companies and surely profited from the volatility.

Our view on all of this is that no one really knows what the true impact of AI will be on the economy and markets over time, and trying to trade on it is a fool’s errand. There will be winners and losers; our focus has been on the companies providing the “picks and shovels” or the “plumbing” around the technology. As noted above, we are finding opportunities to make direct investments in AI-adjacent areas where we partner with managers with the knowledge and experience to profit in this space both on the long and short sides of the portfolio.

* * *

We have been writing about AI in our recent letters, and our use of the tools and talking to other investors who have leaned into the technology have taught us a few lessons worth sharing. One is the power of a good prompt: Writing more effective AI prompts leads to better results because clear, specific instructions help the model understand exactly what you want. A strong prompt gives useful context, defines the task, sets the tone or format, and may include constraints like length, audience, or examples. The more precise the prompt, the less the AI has to guess, which usually means responses that are more accurate, relevant, and usable. At the end of this letter, we have included a list of tips for writing good AI prompts.

We welcome any thoughts you may have.

Sincerely,

Alternative Investment Management, LLC (AIM13)