AIM13 Commentary - 2026 Q1

“Don’t confuse luck with skill when judging others, and especially when judging yourself”

With markets soaring, someone asks us almost every day, will the market crash? Our answer is, with 100% certainty, yes, THE MARKET WILL CRASH. We are then asked, WHEN?? And our answer, again with 100% certainty, is WE HAVE NO IDEA! This leaves people a little unsatisfied. So let us be very clear and issue a warning in no uncertain terms: A MARKET GOING STRAIGHT UP WILL NOT LAST FOREVER. While a lot of people think investing today is “easy,” we think quite the opposite: Investing today is harder than ever. More on that below.

Unfortunately, as we have written before, people tend not to be honest with themselves and confuse a bull market with being a great investor. At a recent dinner, someone suggested to type "Roast me" into ChatGPT. It provided a humorous (but frighteningly accurate) description of who we are. We encourage you to do this not only for fun but to give yourself a perspective you might not see, especially when it comes to investing. Everyone needs to be their own toughest critic as it is human nature to give yourself all the credit for winners but find excuses beyond your control for your investment losers.

Looking at the markets in the first quarter, we observed again people also making the mistake of getting caught up in measuring performance over short time periods, which can disguise real returns. For instance, in the month of March, the S&P 500 TR was down -5.0%, a big down month. Yet had the 31-day period shifted back just one day to end March 30, the S&P would have been down over 8%. And had it been shifted forward nine days to end April 9, it would have been up 50 bps. The lesson is that calendar month returns are an arbitrary data point with limited utility.

In private equity, while easing interest rates are helping, many private equity investors are frustrated with a backlog of long-hold portfolio companies. Continuation vehicles, secondaries, and similar mechanisms continue to grow, and we have been spending time on how best to take advantage of the dynamics of LPs needing liquidity versus GPs wishing to hold assets longer. As we noted last quarter, unlike for many PE investors, our distribution pace has materially picked up, which we think is a function of our focus on the small to mid-size managers who sell up to the biggest funds where the illiquidity problem is most pronounced.

* * *

“This ship can’t sink!”

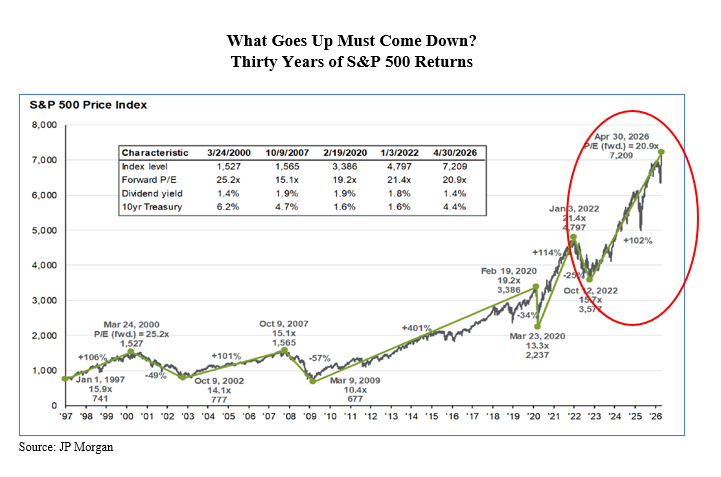

We realized recently that if you are an investor and you are forty years old – a time when you are really hitting your stride – you were just graduating from college when the market crashed during the Great Financial Crisis. Moreover, you never sustained a market correction during your working career. So you might not be faulted for thinking that the market always goes up, or when it goes down, the drop is shallow and it quickly recovers. Recent experience certainly bears this out:

We live in an almost unprecedented time, to put it mildly. Here are just a few quick datapoints on just how unusual today’s investing environment is:

S&P 500 TR returns are at unhistoric levels:

In the last three years, annualized S&P 500 TR returns have been about 23%.

The ten-year return number stands at about 15%.

Lifetime S&P annualized returns are more like 10%.

The U.S. total market cap to GDP ratio – aka the "Buffett Indicator" – is off the charts:

The ratio currently sits at approximately 234%, a record high.

The historical median is 81%.

Warren Buffett said in 2001 that "if the ratio approaches 200%, you are playing with fire."

Another valuation measure, the CAPE ratio (which is the cyclically adjusted price-to-earnings ratio) is flashing warning signals as well:

Currently the ratio sits at 42:1. There have only been two other times in history when the ratio touched 40 to 1: 1929 and 1999.

Even Treasuries are in rare territory:

The 30-year Treasury yield recently hit its highest level since 2007.

At the same time, stock-yield correlation recently fell to -0.68, its lowest level since September 1999.

Not surprising, IPO’s are back, with SpaceX, expected to be the largest in history (by a factor of three), slated for mid-June. The era of the trillion dollar IPO is upon us.

“Life is just a party, and parties weren’t meant to last.”

In periods like these of sustained market strength, when markets climb steadily and nearly every portfolio tells a story of success, it is tempting to believe that skill and luck are one and the same. A rising tide lifts all boats, and in moments like these, it can be difficult to distinguish the disciplined navigator from the one simply carried by the current. Yet it is precisely in these euphoric conditions — not in the downturns — that the true test of an investment manager reveals itself. The best managers resist the pull of momentum, ask hard questions when the crowd is celebrating, and remain anchored to process and fundamentals when patience feels like a penalty.

“Don’t confuse brains with a bull market.”

While many people think that investing today is easy, that opportunities to make money are plentiful, and that little or no skill is required to generate great returns, we think quite the opposite. Investing in the equity markets today is harder than ever. Why? Below are some parts of our investment process that are particularly challenging in today’s environment:

Protecting capital: Staying diversified is an important part of protecting capital, and hedged equity is only a portion of our overall portfolio, with cash, private investments (PE, VC, credit, etc.) and other investments intended to provide uncorrelated returns when things get tough in public equity. When hedge fund performance lagged the general markets a few years ago, we were OK with it as other parts of our portfolio outperformed. In today’s environment, however, we are spending more time to ensure that the public portfolio has adequate protection such as by doing the following, among other things:

Using cash to dampen volatility and provide a reserve to add opportunistically when managers are down.

Finding managers who can short well (typically the smaller ones).

Trimming winners to maintain an adequately diversified portfolio

Selecting managers: Everyone looks like a genius when all markets are rising, but who are the ones who will perform equally well when times are tough? When times are good, selecting managers is harder because you need to strip out the good investment performance and analyze other things. When times are tough, the true measure of a manager’s investment skill is more apparent. Similarly, sometimes the best (but the hardest) thing to do is to do nothing, and not many active managers understand that – especially when everything that they do works.

“Success breeds complacency. Complacency breeds failure.

Only the paranoid survive.”

Maintaining rigorous due diligence. When managers generate market returns in a rising tape, fewer questions get asked and less attention is spent on the manager, both from an investment and non-investment perspective. Complacency is the bane of good investing. Nothing is dumber than lessening scrutiny of managers and deals just because they have been performing well – past performance is not necessarily indicative of future returns!

Staying focused: Every day we are bombarded with new deals, new funds, and new opportunities. Where AI should help us more quickly separate the good from the bad – the quick “no” always being the second best answer for a manager – it is harder than ever to narrow down what is actionable. And as we see potential home runs almost everyday, there is also a tendency to fall victim to a FOMO mentality. Having lived through other boom/bust cycles, staying disciplined and focused is the hardest when times are good.

“Better three hours too soon than a minute too late.”

We have often said that the good thing about being bearish is you are never wrong, just early. At the end of the day, it is not what you make but how you make it that matters, and in today’s environment, too many people think that investing is easy. They lose sight of how they are making their returns.

Market Observations

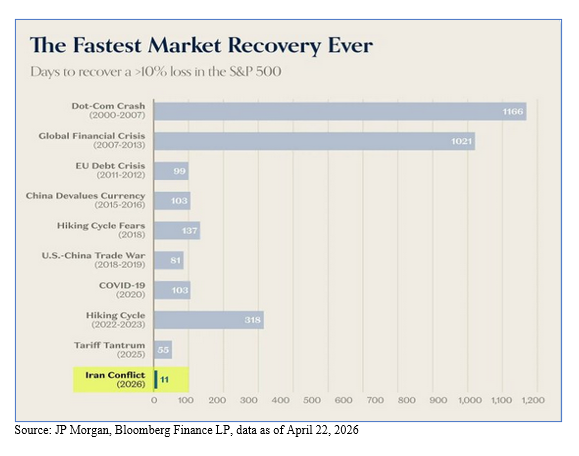

We said above that we know the market will crash, but just not when. The resilience of the markets continues to surprise us, and it was illustrated by an interesting chart shared with us recently by one of our partners:

Against a backdrop of everything seemingly being OK and business as usual, we continue to identify things that either cause us to scratch our head or, worse, keep us up at night:

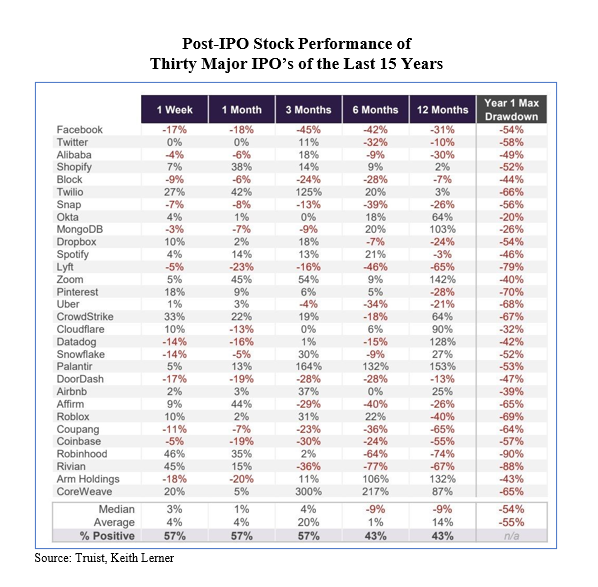

The return of the IPO: Buyer beware! As we write this letter, SpaceX has just completed the largest IPO in the history of Wall Street, and other firms like OpenAI and Anthropic are poised to go public – adding over $4 trillion in market capitalization to the public equity markets. Many investors are getting calls from their brokers on how to get in, which reminds us (very troublingly) of 1999. Before being swept up in the mania, it is important to remember that IPO stock performance post-IPO has been mixed at best:

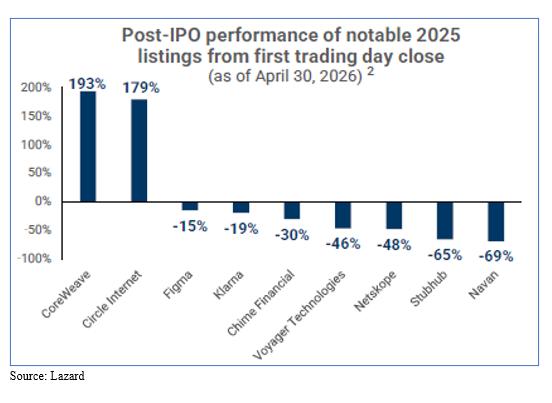

Even IPO’s from 2025, which have enjoyed a supportive market environment have had trouble sustaining their IPO price:

The lesson here is that you never believe someone when they say, “this time is different.” As we said above, resist the FOMO urge.

Partners Group limiting withdrawals. On June 3rd, Partners Group, one of the largest private markets investment firms in the world, capped redemptions on its flagship evergreen private equity fund, triggering a 17% collapse in its share price. This was the worst single-day drop since it went public in 2006. The firm told investors that withdrawals from the fund would be limited to 5% of net asset value per quarter, after requests reached an estimated 9.8% in Q2 2026. We have long been skeptics of many so-called “evergreen funds,” as we are convinced that managers do not always manage the “asset-liability” mismatch when it comes to liquidity. Unfortunately, these strategies have been sold to thousands of retail investors who likely did not understand how liquidity worked in times of stress.

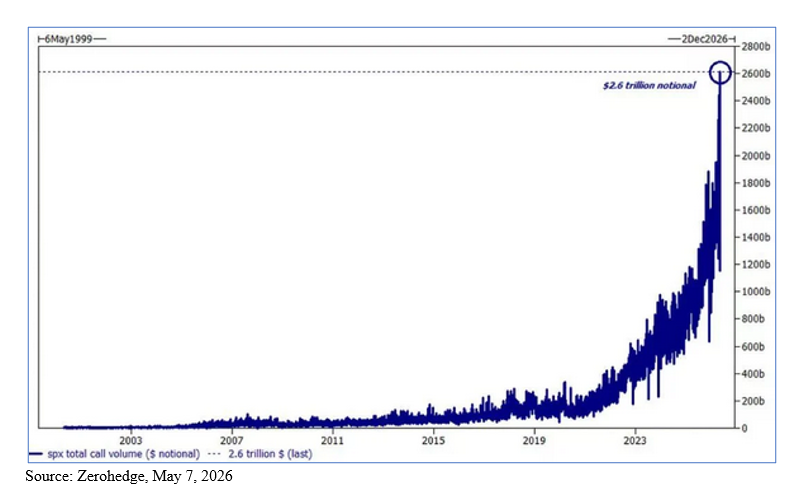

Call options on the S&P 500 reach record levels. In early May, single day call option buying reached $2.6 trillion, the highest level on record:

Aside from another indicatioin of extreme bullishness, why does this matter? As investors buy more and more call options, market makers must hedge their exposure by buying the corresponding stocks. This is known as a “gamma squeeze” where momentum option buying applies equal pressure on stock buying (think GameStop in January 2021). Can this last forever? Of course not, as all option contracts have expiration dates. However, the higher the stakes, the crazier the market becomes. The crazier the market gets, the more people gamble. We have seen this before. It has nothing to do with fundamentals, and it does not end well.

Closing Thought: Investing in today’s geopolitical environment

In the middle of April, Carlyle’s CEO, Harvey Schwartz, made headlines at Semafor’s World Economy Summit when he said that markets are mispricing geopolitical risks. Investors have “gotten accustomed to very unsettling geopolitical events sorting themselves out,” he said, leading many to be complacent about the gravity of such risks. We agree. Readers of our letters know that for a long time we have viewed the geopolitical environment as an important driver of investment risk and returns. We spend a lot of time talking to our hedged equity, private equity, and venture managers about how they are thinking about the geopolitical environment and have invested in areas critical to our nation’s independence and survival. Ignoring the geopolitical environment or downplaying any associated risks is dangerous, both to one’s investment portfolio and, more importantly, to one’s own safety and that of one’s family and friends.

* * *

Sincerely,

Alternative Investment Management, LLC (AIM13)